Finance:Market (economics)

| Part of a series on |

| Economics |

|---|

|

|

| Financial markets |

|---|

|

| Bond market |

| Stock market |

| Other markets |

| Over-the-counter (off-exchange) |

| Trading |

| Related areas |

A market is one of the many varieties of systems, institutions, procedures, social relations and infrastructures whereby parties engage in exchange. While parties may exchange goods and services by barter, most markets rely on sellers offering their goods or services (including labor) in exchange for money from buyers. It can be said that a market is the process by which the prices of goods and services are established. Markets facilitate trade and enable the distribution and resource allocation in a society. Markets allow any trade-able item to be evaluated and priced. A market emerges more or less spontaneously or may be constructed deliberately by human interaction in order to enable the exchange of rights (cf. ownership) of services and goods. Markets generally supplant gift economies and are often held in place through rules and customs, such as a booth fee, competitive pricing, and source of goods for sale (local produce or stock registration).

Markets can differ by products (goods, services) or factors (labour and capital) sold, product differentiation, place in which exchanges are carried, buyers targeted, duration, selling process, government regulation, taxes, subsidies, minimum wages, price ceilings, legality of exchange, liquidity, intensity of speculation, size, concentration, exchange asymmetry, relative prices, volatility and geographic extension. The geographic boundaries of a market may vary considerably, for example the food market in a single building, the real estate market in a local city, the consumer market in an entire country, or the economy of an international trade bloc where the same rules apply throughout. Markets can also be worldwide, see for example the global diamond trade. National economies can also be classified as developed markets or developing markets.

In mainstream economics, the concept of a market is any structure that allows buyers and sellers to exchange any type of goods, services and information. The exchange of goods or services, with or without money, is a transaction.[1] Market participants consist of all the buyers and sellers of a good who influence its price, which is a major topic of study of economics and has given rise to several theories and models concerning the basic market forces of supply and demand. A major topic of debate is how much a given market can be considered to be a "free market", that is free from government intervention. Microeconomics traditionally focuses on the study of market structure and the efficiency of market equilibrium; when the latter (if it exists) is not efficient, then economists say that a market failure has occurred. However it is not always clear how the allocation of resources can be improved since there is always the possibility of government failure.

Types of markets

A market is one of the many varieties of systems, institutions, procedures, social relations and infrastructures whereby parties engage in exchange. While parties may exchange goods and services by barter, most markets rely on sellers offering their goods or services (including labor) in exchange for money from buyers. It can be said that a market is the process by which the prices of goods and services are established. Markets facilitate trade and enables the distribution and allocation of resources in a society. Markets allow any trade-able item to be evaluated and priced. A market sometimes emerges more or less spontaneously or may be constructed deliberately by human interaction in order to enable the exchange of rights (cf. ownership) of services and goods.

Markets of varying types can spontaneously arise whenever a party has interest in a good or service that some other party can provide. Hence there can be a market for cigarettes in correctional facilities, another for chewing gum in a playground, and yet another for contracts for the future delivery of a commodity. There can be black markets, where a good is exchanged illegally, for example markets for goods under a command economy despite pressure to repress them and virtual markets, such as eBay, in which buyers and sellers do not physically interact during negotiation. A market can be organized as an auction, as a private electronic market, as a commodity wholesale market, as a shopping center, as a complex institution such as a stock market and as an informal discussion between two individuals.

Markets vary in form, scale (volume and geographic reach), location and types of participants as well as the types of goods and services traded. The following is a non exhaustive list:

Physical consumer markets

- Food retail markets: farmers' markets, fish markets, wet markets and grocery stores

- Retail marketplaces: public markets, market squares, Main Streets, High Streets, bazaars, souqs, night markets, shopping strip malls and shopping malls

- Big-box stores: supermarkets, hypermarkets and discount stores

- Ad hoc auction markets: process of buying and selling goods or services by offering them up for bid, taking bids and then selling the item to the highest bidder

- Used goods markets such as flea markets

- Temporary markets such as fairs

Physical business markets

- Physical wholesale markets: sale of goods or merchandise to retailers; to industrial, commercial, institutional, or other professional business users or to other wholesalers and related subordinated services

- Markets for intermediate goods used in production of other goods and services

- Labor markets: where people sell their labour to businesses in exchange for a wage

- Ad hoc auction markets: process of buying and selling goods or services by offering them up for bid, taking bids and then selling the item to the highest bidder

- Temporary markets such as trade fairs

Non-physical markets

- Media markets (broadcast market): is a region where the population can receive the same (or similar) television and radio station offerings and may also include other types of media including newspapers and Internet content

- Internet markets (electronic commerce): trading in products or services using computer networks, such as the Internet

- Artificial markets created by regulation to exchange rights for derivatives that have been designed to ameliorate externalities, such as pollution permits (see carbon trading)

Financial markets

Financial markets facilitate the exchange of liquid assets. Most investors prefer investing in two markets:

- The stock markets, for the exchange of shares in corporations (NYSE, AMEX and the NASDAQ are the most common stock markets in the United States)

- The bond markets

There are also:

- Currency markets are used to trade one currency for another, and are often used for speculation on currency exchange rates

- The money market is the name for the global market for lending and borrowing

- Futures markets, where contracts are exchanged regarding the future delivery of goods are often an outgrowth of general commodity markets

- Prediction markets are a type of speculative market in which the goods exchanged are futures on the occurrence of certain events; they apply the market dynamics to facilitate information aggregation

Unauthorized and illegal markets

- Grey markets (parallel markets): is the trade of a commodity through distribution channels which, while legal, are unofficial, unauthorized, or unintended by the original manufacturer[citation needed]

- markets in illegal goods such as the market for illicit drugs, illegal arms, infringing products, cigarettes sold to minors or untaxed cigarettes (in some jurisdictions), or the private sale of unpasteurized goat milk[2]

Mechanisms of markets

In economics, a market that runs under laissez-faire policies is called a free market, it is "free" from the government, in the sense that the government makes no attempt to intervene through taxes, subsidies, minimum wages, price ceilings and so on. However, market prices may be distorted by a seller or sellers with monopoly power, or a buyer with monopsony power. Such price distortions can have an adverse effect on market participant's welfare and reduce the efficiency of market outcomes. The relative level of organization and negotiating power of buyers and sellers also markedly affects the functioning of the market.

Markets are a system and systems have structure. The structure of a well-functioning market is defined by the theory of perfect competition. Well-functioning markets of the real world are never perfect, but basic structural characteristics can be approximated for real world markets, for example:

- Many small buyers and sellers

- Buyers and sellers have equal access to information

- Products are comparable

Markets where price negotiations meet equilibrium, but the equilibrium is not efficient are said to experience market failure. Market failures are often associated with time-inconsistent preferences, information asymmetries, non-perfectly competitive markets, principal–agent problems, externalities, or public goods. Among the major negative externalities which can occur as a side effect of production and market exchange, are air pollution (side-effect of manufacturing and logistics) and environmental degradation (side-effect of farming and urbanization).

There exists a popular thought, especially among economists, that free markets would have a structure of a perfect competition.[citation needed] The logic behind this thought is that market failures are thought to be caused by other exogenic systems, and after removing those exogenic systems ("freeing" the markets) the free markets could run without market failures.[citation needed] For a market to be competitive, there must be more than a single buyer or seller. It has been suggested that two people may trade, but it takes at least three persons to have a market, so that there is competition in at least one of its two sides.[3] However, competitive markets—as understood in formal economic theory—rely on much larger numbers of both buyers and sellers. A market with a single seller and multiple buyers is a monopoly. A market with a single buyer and multiple sellers is a monopsony. These are "the polar opposites of perfect competition".[4] As an argument against such a logic, there is a second view that suggests that the source of market failures is inside the market system itself, therefore the removal of other interfering systems would not result in markets with a structure of perfect competition. As an analogy, such an argument may suggest that capitalists do not want to enhance the structure of markets, just like a coach of a football team would influence the referees or would break the rules if he could while he is pursuing his target of winning the game. Thus according to this view, capitalists are not enhancing the balance of their team versus the team of consumer-workers, so the market system needs a "referee" from outside that balances the game. In this second framework, the role of a "referee" of the market system is usually to be given to a democratic government.

Study of markets

_002.jpg)

Disciplines such as sociology, economic history, economic geography and marketing developed novel understandings of markets[5] studying actual existing markets made up of persons interacting in diverse ways in contrast to an abstract and all-encompassing concepts of "the market". The term "the market" is generally used in two ways:

- "The market" denotes the abstract mechanisms whereby supply and demand confront each other and deals are made; in its place, reference to markets reflects ordinary experience and the places, processes and institutions in which exchanges occurs[6]

- "The market" signifies an integrated, all-encompassing and cohesive capitalist world economy.

Economics

Microeconomics (from Greek prefix mikro- meaning "small" and economics) is a branch of economics that studies the behavior of individuals and small impacting organizations in making decisions on the allocation of limited resources (see scarcity). On the other hand, macroeconomics (from the Greek prefix makro- meaning "large" and economics) is a branch of economics dealing with the performance, structure, behavior and decision-making of an economy as a whole, rather than individual markets.

The modern field of microeconomics arose as an effort of neoclassical economics school of thought to put economic ideas into mathematical mode. It began in the 19th century debates surrounding the works of Antoine Augustine Cournot, William Stanley Jevons, Carl Menger and Léon Walras—this period is usually denominated as the Marginal Revolution. A recurring theme of these debates was the contrast between the labor theory of value and the subjective theory of value, the former being associated with classical economists such as Adam Smith, David Ricardo and Karl Marx (Marx was a contemporary of the marginalists).

In his Principles of Economics (1890),[7] Alfred Marshall presented a possible solution to this problem, using the supply and demand model. Marshall's idea of solving the controversy was that the demand curve could be derived by aggregating individual consumer demand curves, which were themselves based on the consumer problem of maximizing utility. The supply curve could be derived by superimposing a representative firm supply curves for the factors of production and then market equilibrium would be given by the intersection of demand and supply curves. He also introduced the notion of different market periods: mainly long run and short run. This set of ideas gave way to what economists call perfect competition—now found in the standard microeconomics texts—even though Marshall himself was highly skeptical, it could be used as general model of all markets.

Opposed to the model of perfect competition, some models of imperfect competition were proposed:

- The monopoly model, already considered by marginalist economists, describes a profit maximizing capitalist facing a market demand curve with no competitors, who may practice price discrimination.

- Oligopoly is a market form in which a market or industry is dominated by a small number of sellers. The oldest model was the duopoly of Cournot (1838).[8] It was criticized by Harold Hotelling for its instability, by Joseph Bertrand for lacking equilibrium for prices as independent variables. Hotelling built a model of market located over a line with two sellers in each extreme of the line, in this case maximizing profit for both sellers leads to a stable equilibrium. From this model also follows that if a seller is to choose the location of his store so as to maximize his profit, he will place his store the closest to his competitor as "the sharper competition with his rival is offset by the greater number of buyers he has an advantage".[9] He also argues that clustering of stores is wasteful from the point of view of transportation costs and that public interest would dictate more spatial dispersion.

- Monopolistic competition is a type of imperfect competition such that many producers sell products that are differentiated from one another (e.g. by branding or quality) and hence are not perfect substitutes. In monopolistic competition, a firm takes the prices charged by its rivals as given and ignores the impact of its own prices on the prices of other firms. The "founding father" of the theory of monopolistic competition is Edward Hastings Chamberlin, who wrote a pioneering book on the subject, Theory of Monopolistic Competition (1933). Joan Robinson published a book called The Economics of Imperfect Competition with a comparable theme of distinguishing perfect from imperfect competition. Chamberlin defined monopolistic competition as "challenge to traditional viewpoint of economics that competition and monopoly are alternatives and that individual prices are to be explained in terms of one or the other". He continues: "By contrast it is held that most economic situations are composite of both competition and monopoly, and that, wherever this is the case, a false view is given by neglecting either one of the two forces and regarding the situation as made up entirely of the other".[10]

William Baumol provided in his 1977 paper[11] the current formal definition of a natural monopoly where “an industry in which multiform production is more costly than production by a monopoly”. Baumol defined a contestable market in his 1982 paper as a market where "entry is absolutely free and exit absolutely costless", freedom of entry in Stigler sense: the incumbent has no cost discrimination against entrants. He states that a contestable market will never have an economic profit greater than zero when in equilibrium and the equilibrium will also be efficient. According to Baumol, this equilibrium emerges endogenously due to the nature of contestable markets, that is the only industry structure that survives in the long run is the one which minimizes total costs. This is in contrast to the older theory of industry structure since not only industry structure is not exogenously given, but equilibrium is reached without add hoc hypothesis on the behavior of firms, say using reaction functions in a duopoly. He concludes the paper commenting that regulators that seek to impede entry and/or exit of firms would do better to not interfere if the market in question resembles a contestable market.

Around the 1970s the study of market failures came into focus with the study of information asymmetry. In particular, three authors emerged from this period: Akerlof, Spence and Stiglitz. Akerlof considered the problem of bad quality cars driving good quality cars out of the market in his classic "The Market for Lemons" (1970) because of the presence of asymmetrical information between buyers and sellers.[12] Michael Spence explained that signaling was fundamental in the labour market because since employers can't know beforehand which candidate is the most productive, a college degree becomes a signaling device that a firm uses to select new personnel.[13]

C. B. Macpherson identifies an underlying model of the market underlying Anglo-American liberal democratic political economy and philosophy in the seventeenth and eighteenth centuries: persons are cast as self-interested individuals, who enter into contractual relations with other such individuals, concerning the exchange of goods or personal capacities cast as commodities, with the motive of maximizing pecuniary interest. The state and its governance systems are cast as outside of this framework.[14] This model came to dominant economic thinking in the later nineteenth century, as economists such as Ricardo, Mill, Jevons, Walras and later neo-classical economics shifted from reference to geographically located marketplaces to an abstract "market".[15] This tradition is continued in contemporary neoliberalism, where the market is held up as optimal for wealth creation and human freedom and the states' role imagined as minimal, reduced to that of upholding and keeping stable property rights, contract and money supply. According to David Harvey, this allowed for boilerplate economic and institutional restructuring under structural adjustment and post-Communist reconstruction.[16] Similar formalism occurs in a wide variety of social democratic and Marxist discourses that situate political action as antagonistic to the market. In particular, commodification theorists such as György Lukács insist that market relations necessarily lead to undue exploitation of labour and so need to be opposed in toto.[17]

A central theme of empirical analyses is the variation and proliferation of types of markets since the rise of capitalism and global scale economies. The Regulation school stresses the ways in which developed capitalist countries have implemented varying degrees and types of environmental, economic and social regulation, taxation and public spending, fiscal policy and government provisioning of goods, all of which have transformed markets in uneven and geographical varied ways and created a variety of mixed economies.

Drawing on concepts of institutional variance and path dependence, varieties of capitalism theorists (such as Peter Hall and David Soskice) identify two dominant modes of economic ordering in the developed capitalist countries, "coordinated market economies" such as Germany and Japan and an Anglo-American "liberal market economies". However, such approaches imply that the Anglo-American liberal market economies in fact operate in a matter close to the abstract notion of "the market". While Anglo-American countries have seen increasing introduction of neo-liberal forms of economic ordering, this has not led to simple convergence, but rather a variety of hybrid institutional orderings.[18] Rather, a variety of new markets have emerged, such as for carbon trading or rights to pollute. In some cases, such as emerging markets for water, different forms of privatization of different aspects of previously state run infrastructure have created hybrid private-public formations and graded degrees of commodification, commercialization, and privatization.[19]

Marketing

This section may need to be rewritten to comply with Wikipedia's quality standards. (February 2018) |

The marketing management school, evolved in the late 1950s and early 1960s, is fundamentally linked with the marketing mix[20] framework, a business tool used in marketing and by marketers. In his paper "The Concept of the Marketing Mix", Neil H. Borden reconstructed the history of the term "marketing mix".[21][22] He started teaching the term after an associate, James Culliton, described the role of the marketing manager in 1948 as a "mixer of ingredients"; one who sometimes follows recipes prepared by others, sometimes prepares his own recipe as he goes along, sometimes adapts a recipe from immediately available ingredients, and at other times invents new ingredients no one else has tried. The marketer E. Jerome McCarthy proposed a four Ps classification (product, price, promotion, place) in 1960, which has since been used by marketers throughout the world.[23] Robert F. Lauterborn proposed a four Cs classification (consumer, price, promotion, place) in 1990 which is a more consumer-oriented version of the four Ps that attempts to better fit the movement from mass marketing to niche marketing.[24] Koichi Shimizu proposed a 7Cs Compass Model (corporation, commodity, cost, communication, channel, consumer, circumstances) to provide a more complete picture of the nature of marketing in 1981.

Businesses market their products/services to a specific segments of consumers. The defining factors of the markets are determined by demographics, interests and age/gender. A form of expansion is to enter a new market and sell/advertise to a different set of users.

Sociology

A prominent entry-point for challenging the market model's applicability concerns exchange transactions and the homo economicus assumption of self-interest maximization. As of 2012[update], a number of streams of economic sociological analysis of markets focus on the role of the social in transactions and on the ways transactions involve social networks and relations of trust, cooperation and other bonds.[25] Economic geographers in turn draw attention to the ways exchange transactions occur against the backdrop of institutional, social and geographic processes, including class relations, uneven development and historically contingent path-dependencies.[26] Pierre Bourdieu has suggested the market model is becoming self-realizing in virtue of its wide acceptance in national and international institutions through the 1990s.[27]

Michel Callon's concept of framing provides a useful schema: each economic act or transaction occurs against, incorporates and also re-performs a geographically and cultural specific complex of social histories, institutional arrangements, rules and connections. These network relations are simultaneously bracketed, so that persons and transactions may be disentangled from thick social bonds. The character of calculability is imposed upon agents as they come to work in markets and are “formatted” as calculative agencies. Market exchanges contain a history of struggle and contestation that produced actors predisposed to exchange under certain sets of rules. Therefore, for Challon, market transactions can never be disembedded from social and geographic relations and there is no sense to talking of degrees of embeddedness and disembeddeness.[28] An emerging theme is the interrelationship, inter-penetrability and variations of concepts of persons, commodities and modes of exchange under particular market formations. This is most pronounced in recent movement towards post-structuralist theorizing that draws on Michel Foucault and Actor Network Theory and stress relational aspects of person-hood, and dependence and integration into networks and practical systems. Commodity network approaches further both deconstruct and show alternatives to the market models concept of commodities.[29]

In social systems theory (cf. Niklas Luhmann), markets are also conceptualized as inner environments of the economy. As horizon of all potential investment decisions the market represents the environment of the actually realized investment decisions. However, such inner environments can also be observed in further function systems of society like in political, scientific, religious or mass media systems.[30]

Economic geography

A widespread trend in economic history and sociology is skeptical of the idea that it is possible to develop a theory to capture an essence or unifying thread to markets.[31] For economic geographers, reference to regional, local, or commodity specific markets can serve to undermine assumptions of global integration and highlight geographic variations in the structures, institutions, histories, path dependencies, forms of interaction and modes of self-understanding of agents in different spheres of market exchange.[32] Reference to actual markets can show capitalism not as a totalizing force or completely encompassing mode of economic activity, but rather as "a set of economic practices scattered over a landscape, rather than a systemic concentration of power".[33]

Problematic for market formalism is the relationship between formal capitalist economic processes and a variety of alternative forms, ranging from semi-feudal and peasant economies widely operative in many developing economies, to informal markets, barter systems, worker cooperatives, or illegal trades that occur in most developed countries. Practices of incorporation of non-Western peoples into global markets in the nineteenth and twentieth century did not merely result in the quashing of former social economic institutions. Rather, various modes of articulation arose between transformed and hybridized local traditions and social practices and the emergent world economy. By their liberal nature, so called capitalist markets have almost always included a wide range of geographically situated economic practices that do not follow the market model. Economies are thus hybrids of market and non-market elements.[34]

Helpful here is J. K. Gibson-Graham's complex topology of the diversity of contemporary market economies describing different types of transactions, labour and economic agents. Transactions can occur in black markets (such as for marijuana) or be artificially protected (such as for patents). They can cover the sale of public goods under privatization schemes to co-operative exchanges and occur under varying degrees of monopoly power and state regulation. Likewise, there are a wide variety of economic agents, which engage in different types of transactions on different terms: one cannot assume the practices of a religious kindergarten, multinational corporation, state enterprise, or community-based cooperative can be subsumed under the same logic of calculability. This emphasis on proliferation can also be contrasted with continuing scholarly attempts to show underlying cohesive and structural similarities to different markets.[25] Gibson-Graham thus read a variety of alternative markets for fair trade and organic foods or those using local exchange trading system as not only contributing to proliferation, but also forging new modes of ethical exchange and economic subjectivities.

Anthropology

Economic anthropology is a scholarly field that attempts to explain human economic behavior in its widest historic, geographic and cultural scope. It is practiced by anthropologists and has a complex relationship with the discipline of economics, of which it is highly critical.[citation needed]

Its origins as a sub-field of anthropology begin with the Polish-British founder of anthropology, Bronisław Malinowski, and his French compatriot, Marcel Mauss, on the nature of gift-giving exchange (or reciprocity) as an alternative to market exchange. Studies in economic anthropology for the most part are focused on exchange. Bronisław Malinowski's path-breaking work, Argonauts of the Western Pacific (1922), addressed the question "why would men risk life and limb to travel across huge expanses of dangerous ocean to give away what appear to be worthless trinkets?". Malinowski carefully traced the network of exchanges of bracelets and necklaces across the Trobriand Islands and established that they were part of a system of exchange (the Kula ring). He stated that this exchange system was clearly linked to political authority.[35] In the 1920s and later, Malinowski's study became the subject of debate with the French anthropologist, Marcel Mauss, author of The Gift (Essai sur le don, 1925).[36] Malinowski emphasized the exchange of goods between individuals and their non-altruistic motives for giving: they expected a return of equal or greater value (colloquially referred to as "Indian giving"). In other words, reciprocity is an implicit part of gifting as no "free gift" is given without expectation of reciprocity. In contrast, Mauss has emphasized that the gifts were not between individuals, but between representatives of larger collectivities. He argued these gifts were a "total prestation" as they were not simple, alienable commodities to be bought and sold, but like the "Crown jewels" embodied the reputation, history and sense of identity of a "corporate kin group", such as a line of kings. Given the stakes, Mauss asked "why anyone would give them away?" and his answer was an enigmatic concept, "the spirit of the gift". A good part of the confusion (and resulting debate) was due to a bad translation. Mauss appeared to be arguing that a return gift is given to keep the very relationship between givers alive; a failure to return a gift ends the relationship; and the promise of any future gifts. Based on an improved translate, Jonathan Parry has demonstrated that Mauss was arguing that the concept of a "pure gift" given altruistically only emerges in societies with a well-developed market ideology.[35]

Rather than emphasize how particular kinds of objects are either gifts or commodities to be traded in restricted spheres of exchange, Arjun Appadurai and others began to look at how objects flowed between these spheres of exchange. They shifted attention away from the character of the human relationships formed through exchange and placed it on "the social life of things" instead. They examined the strategies by which an object could be "singularized" (made unique, special, one-of-a-kind) and so withdrawn from the market. A marriage ceremony that transforms a purchased ring into an irreplaceable family heirloom is one example whereas the heirloom in turn makes a perfect gift.

Mathematical modeling

Although arithmetic has been used since the beginning of civilization to set prices, it was not until the 19th century that more advanced mathematical tools began to be used to study markets in the form of social statistics. More recent techniques include business intelligence, data mining and marketing engineering.

Size parameters

Market size can be given in terms of the number of buyers and sellers in a particular market[37] or in terms of the total exchange of money in the market, generally annually (per year). When given in terms of money, market size is often termed "market value", but in a sense distinct from market value of individual products. For one and the same goods, there may be different (and generally increasing) market values at the production level, the wholesale level and the retail level. For example, the value of the global illicit drug market for the year 2003 was estimated by the United Nations to be US$13 billion at the production level, $94 billion at the wholesale level (taking seizures into account) and US$322 billion at the retail level (based on retail prices and taking seizures and other losses into account).[38]

-

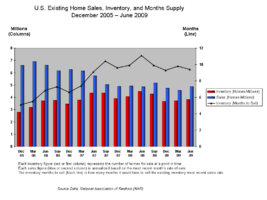

United States home sales (blue)

United States home sales (blue) -

Book Sales in the United Kingdom

Book Sales in the United Kingdom -

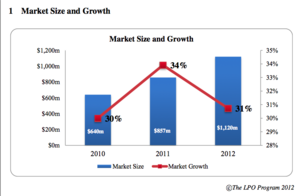

Size and growth of the legal outsourcing market

Size and growth of the legal outsourcing market -

Global mobiles applications market size

Global mobiles applications market size

See also

References

- ↑ "Transaction", Oxford Dictionaries. Retrieved 25 October 2014.

- ↑ Heyne, Paul; Boettke, Peter J.; Prychitko, David L. (2014). The Economic Way of Thinking (13th ed.). Pearson. pp. 130–132. ISBN 978-0-13-299129-2.

- ↑ O'Sullivan, Arthur; Sheffrin, Steven M. (2003). Economics: Principles in Action. Upper Saddle River, New Jersey: Pearson Prentice Hall. p. 28. ISBN 0-13-063085-3.

- ↑ Robert S. Pindyck, Daniel L. Rubinfeld, Microeconomics, Pearson International Edition 2009

- ↑ Diaz Ruiz, C. A. (2012). "Theories of markets: Insights from marketing and the sociology of markets". The Marketing Review 12 (1): 61–77. doi:10.1362/146934712X13286274424316.

- ↑ Callon, M. (1998) "Introduction: The Embeddedness of Economic Markets in Economics." In The Laws of the Markets, edited by Michel Callon. Basic Blackwell/The Sociological Review pp. 1–57 1998, p.2).

- ↑ A. Marshall, Principles of Economics, 1890

- ↑ A. Cournot, Researches into the mathematical principles of the theory of wealth, 1838 https://archive.org/details/researchesintom00fishgoog

- ↑ Hotteling, H. (1929). "Stability in Competition". The Economic Journal 39 (153): 41–57. doi:10.2307/2224214.

- ↑ Chamberlin, E. H. (1937). "Monopolistic or Imperfect Competition?". The Quarterly Journal of Economics 51 (4): 557–580. doi:10.2307/1881679.

- ↑ Baumol, William J. (1977). "On the Proper Cost Tests for Natural Monopoly in a Multiproduct Industry". American Economic Review 67 (5): 809–822.

- ↑ Akerlof, George A. (1970). "The Market for ‘Lemons’: Quality Uncertainty and the Market Mechanism". Quarterly Journal of Economics 84 (3): 488–500. doi:10.2307/1879431.

- ↑ Spence, A. M. (1973). "Job Market Signaling". Quarterly Journal of Economics 87 (3): 355–374. doi:10.2307/1882010.

- ↑ MacPherson, C.B. (1962) The Political Theory of Possessive Individualism: From Hobbes to Locke. Oxford Clarendon Press. p.3

- ↑ (Swedberg, 1994, p. 258

- ↑ Harvey, David (2005) A Short History of Neoliberalism Oxford University Press.

- ↑ Lukács, György. (1971) History and Class Consciousness. Trans. Rodney Livingstone. Merlin Press. London. p. 87

- ↑ Peck, supra, p. 154)

- ↑ Bakker, Karen (2005) "Neoliberalizing Nature?: Market Environmentalism in water supply in England and Wales" Annals of the Association of American Geographers 95 (3), 542–565

- ↑ Michael J Baker, Michael John Baker, Michael Saren, Marketing Theory: A Student Text, SAGE 2010

- ↑ Borden, Neil. "The Concept of the Marketing Mix". Suman Thapa. https://docs.google.com/viewer?a=v&q=cache:s794cDYCYxAJ:www.commerce.uct.ac.za/managementstudies/Courses/bus2010s/2007/Nicole%2520Frey/Assignments/Borden,%25201984_The%2520concept%2520of%2520marketing.pdf+&hl=en&gl=in&pid=bl&srcid=ADGEESjQD7owLY5RwuEOVer7qeDaZjKIiemGtEMQCTB0amHNizGcuaFQX6t4JMbz2SmtCNc6V3LLp3mAnnZusRcaMpFy-llqtMBHVfMLI26cEVTkx5qFvPIde_At0dNXaIy4Ar0BM6tN&sig=AHIEtbRsrEOiOtAC_eEcBJS0iSRJNlR6Xw. Retrieved 24 April 2013.

- ↑ Borden, Neil H. (1965). "The Concept of the Marketing Mix". in Schwartz, George. Science in marketing. Wiley marketing series. Wiley. p. 286ff. https://books.google.com/books?id=8YJPAAAAMAAJ. Retrieved November 4, 2013.

- ↑ Needham, Dave (1996). Business for Higher Awards. Oxford, England: Heinemann.

- ↑ Lauterborn, B. (1990). New Marketing Litany: Four Ps Passé: C-Words Take Over. Advertising Age, 61(41), 26.

- ↑ 25.0 25.1 Swedberg, 1994, p. 267

- ↑ Martin, Ron (2000) "Institutional Approaches in Economic Geography", Handbook of Economic Geography. Ed. Eric Sheppard and Trevor J. Barnes. Blackwell Publishers.Peck, 2005

- ↑ Bourdieu, Pierre (1999) Acts of Resistance: Against the Tyranny of the Market. The New Press.p. 95

- ↑ Callon, 1998; Mitchell, 2002, p. 291,

- ↑ Hughes, Alex (2005) "Geographies of Exchange and Circulation: alternative trading spaces" Progress in Human Geography

- ↑ Roth, Steffen (2012). "Leaving commonplaces on the common place: Cornerstones of a polyphonic market theory". Journal for Critical Organization Inquiry 10 (3): 43–52.

- ↑ Swedberg, Richard (1994) "Markets as Social Structures" The Handbook of Economic Sociology. Ed. Neil Smelser and Richard Swedberg. Princeton University Press. 255-2821994, p. 258)

- ↑ Peck, J. (2005) "Economic Geographies in Space" Economic Geography 81(2) 129-175.

- ↑ (Gibson-Graham, J.K. (2006) Postcapitalist Politics. University of Minnesota Press,. p. 2).

- ↑ (Mitchell, Timothy (2002) Rule of Experts. University of California Pressp. 270; Gibson-Graham 2006, supra pp. 53–78)

- ↑ 35.0 35.1 Parry, Jonathan (1986). "The Gift, the Indian Gift and the 'Indian Gift'". Man 21 (3): 453–73. doi:10.2307/2803096.

- ↑ Mauss, Marcel (1970). The Gift: Forms and Functions of Exchange in Archaic Societies. London: Cohen & West.

- ↑ investorwords.com > market size Retrieved on April 17, 2010

- ↑ United Nations, "2005 World Drug Report," Office on Drugs and Crime, June 2005, pg. 16. [1]

Further reading

- Pindyck, Robert S. and Daniel L. Rubinfeld, Microeconomics, Prentice Hall 2012.

- Frank, Robert H., Microeconomics and Behavior, 6th ed., McGraw-Hill/Irwin 2006.

- Kotler, P. and Keller, K.L., Marketing Management, Prentice Hall 2011.

- Baker, Michael J. and Michael Saren, Marketing Theory: A Student Text, SAGE 2010. online.

- Aspers, Patrik, Markets, Polity Press 2011. online.

- Bauer, Leonard and Herbert Matis (1988) From moral to political economy: The Genesis of social sciences, History of European Ideas 9 (2), 125–143.

- Nathaus, Klaus and David Gilgen (Eds.), Change of Markets and Market Societies: Concepts and Case Studies. Historical Social Research 36 (3), Special Issue, 2011.

|  |